00015787322022FYfalseP1YP1YP3YP2YP1Y00015787322022-01-012022-12-3100015787322022-06-30iso4217:USD00015787322023-02-23xbrli:shares00015787322022-12-3100015787322021-12-31iso4217:USDxbrli:shares0001578732mmi:RealEstateBrokerageCommissionsMember2022-01-012022-12-310001578732mmi:RealEstateBrokerageCommissionsMember2021-01-012021-12-310001578732mmi:RealEstateBrokerageCommissionsMember2020-01-012020-12-310001578732mmi:FinancingFeesMember2022-01-012022-12-310001578732mmi:FinancingFeesMember2021-01-012021-12-310001578732mmi:FinancingFeesMember2020-01-012020-12-310001578732mmi:OtherRevenuesMember2022-01-012022-12-310001578732mmi:OtherRevenuesMember2021-01-012021-12-310001578732mmi:OtherRevenuesMember2020-01-012020-12-3100015787322021-01-012021-12-3100015787322020-01-012020-12-310001578732us-gaap:PreferredStockMember2019-12-310001578732us-gaap:CommonStockMember2019-12-310001578732us-gaap:AdditionalPaidInCapitalMember2019-12-310001578732us-gaap:ReceivablesFromStockholderMember2019-12-310001578732us-gaap:RetainedEarningsMember2019-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-3100015787322019-12-310001578732us-gaap:RetainedEarningsMember2020-01-012020-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001578732us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001578732us-gaap:CommonStockMember2020-01-012020-12-310001578732us-gaap:ReceivablesFromStockholderMember2020-01-012020-12-310001578732us-gaap:PreferredStockMember2020-12-310001578732us-gaap:CommonStockMember2020-12-310001578732us-gaap:AdditionalPaidInCapitalMember2020-12-310001578732us-gaap:ReceivablesFromStockholderMember2020-12-310001578732us-gaap:RetainedEarningsMember2020-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-3100015787322020-12-310001578732us-gaap:RetainedEarningsMember2021-01-012021-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001578732us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001578732us-gaap:CommonStockMember2021-01-012021-12-310001578732us-gaap:PreferredStockMember2021-12-310001578732us-gaap:CommonStockMember2021-12-310001578732us-gaap:AdditionalPaidInCapitalMember2021-12-310001578732us-gaap:ReceivablesFromStockholderMember2021-12-310001578732us-gaap:RetainedEarningsMember2021-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001578732us-gaap:RetainedEarningsMember2022-01-012022-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001578732us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001578732us-gaap:CommonStockMember2022-01-012022-12-310001578732us-gaap:PreferredStockMember2022-12-310001578732us-gaap:CommonStockMember2022-12-310001578732us-gaap:AdditionalPaidInCapitalMember2022-12-310001578732us-gaap:ReceivablesFromStockholderMember2022-12-310001578732us-gaap:RetainedEarningsMember2022-12-310001578732us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-31mmi:officexbrli:pure0001578732us-gaap:SoftwareDevelopmentMember2022-01-012022-12-310001578732srt:MinimumMember2022-01-012022-12-310001578732srt:MaximumMember2022-01-012022-12-310001578732srt:MinimumMembermmi:LoanToInvestmentSalesAndFinancingProfessionalsMember2022-01-012022-12-310001578732srt:MaximumMembermmi:LoanToInvestmentSalesAndFinancingProfessionalsMember2022-01-012022-12-310001578732mmi:EmployeeStockPurchasePlanMember2022-01-012022-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMembermmi:TransactionRiskMember2022-01-012022-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMembermmi:TransactionRiskMember2020-01-012020-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMembermmi:TransactionRiskMember2021-01-012021-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMemberus-gaap:CustomerConcentrationRiskMember2020-01-012020-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMemberus-gaap:CustomerConcentrationRiskMember2021-01-012021-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMemberus-gaap:CustomerConcentrationRiskMember2022-01-012022-12-310001578732mmi:CustomerMembermmi:CommissionReceivableMemberus-gaap:CustomerConcentrationRiskMember2020-01-012020-12-310001578732mmi:CustomerMembermmi:CommissionReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-01-012022-12-310001578732mmi:CustomerMembermmi:CommissionReceivableMemberus-gaap:CustomerConcentrationRiskMember2021-01-012021-12-310001578732mmi:CustomerMemberus-gaap:SalesRevenueNetMembersrt:MaximumMembercountry:CAus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001578732mmi:CustomerMemberus-gaap:SalesRevenueNetMembersrt:MaximumMembercountry:CAus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001578732mmi:CustomerMemberus-gaap:SalesRevenueNetMembersrt:MaximumMembercountry:CAus-gaap:GeographicConcentrationRiskMember2020-01-012020-12-310001578732us-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2020-01-012020-12-310001578732us-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001578732us-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMemberus-gaap:GeographicConcentrationRiskMember2020-01-012020-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMemberus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001578732us-gaap:SalesRevenueNetMembermmi:CustomerMemberus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-31mmi:Segment0001578732us-gaap:ComputerEquipmentMember2022-12-310001578732us-gaap:ComputerEquipmentMember2021-12-310001578732us-gaap:FurnitureAndFixturesMember2022-12-310001578732us-gaap:FurnitureAndFixturesMember2021-12-310001578732us-gaap:USTreasurySecuritiesMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732us-gaap:AssetBackedSecuritiesMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:ShortTermInvestmentsMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USTreasurySecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:AssetBackedSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMember2022-12-310001578732us-gaap:USTreasurySecuritiesMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732us-gaap:ShortTermInvestmentsMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USTreasurySecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:AssetBackedSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMember2021-12-310001578732us-gaap:USTreasurySecuritiesMember2022-12-310001578732us-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2022-12-310001578732us-gaap:CorporateDebtSecuritiesMember2022-12-310001578732us-gaap:AssetBackedSecuritiesMember2022-12-310001578732us-gaap:USTreasurySecuritiesMember2021-12-310001578732us-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001578732us-gaap:CorporateDebtSecuritiesMember2021-12-310001578732us-gaap:AssetBackedSecuritiesMember2021-12-310001578732srt:MoodysAaaRatingMembersrt:StandardPoorsAARatingMembersrt:FitchAARatingMember2022-01-012022-12-310001578732srt:StandardPoorsAAPlusRatingMembersrt:FitchAAPlusRatingMembermmi:WeightedAverageCreditAaPlusRatingMembersrt:MoodysAa3RatingMember2022-12-31mmi:reportingUnit0001578732us-gaap:AccountingStandardsUpdate201613Member2020-12-310001578732mmi:MortgageServicingRightsNetOfAmortizationMember2022-12-310001578732mmi:MortgageServicingRightsNetOfAmortizationMember2021-12-310001578732mmi:SecurityDepositMember2022-12-310001578732mmi:SecurityDepositMember2021-12-310001578732mmi:EmployeeNotesReceivableMember2022-12-310001578732mmi:EmployeeNotesReceivableMember2021-12-310001578732us-gaap:HeldtomaturitySecuritiesMember2022-12-310001578732us-gaap:HeldtomaturitySecuritiesMember2021-12-310001578732mmi:LoanPerformanceFeeReceivableMember2022-12-310001578732mmi:LoanPerformanceFeeReceivableMember2021-12-310001578732mmi:PrepaidLeaseCostsAndOtherMember2022-12-310001578732mmi:PrepaidLeaseCostsAndOtherMember2021-12-310001578732mmi:MortgageServicingRightsMember2021-12-310001578732us-gaap:StockAppreciationRightsSARSMember2013-03-310001578732us-gaap:StockAppreciationRightsSARSMember2014-01-012014-01-010001578732us-gaap:StockAppreciationRightsSARSMember2022-01-012022-01-010001578732us-gaap:StockAppreciationRightsSARSMember2021-01-012021-01-010001578732us-gaap:StockAppreciationRightsSARSMember2020-01-012020-01-010001578732us-gaap:StockAppreciationRightsSARSMember2022-01-012022-12-310001578732us-gaap:StockAppreciationRightsSARSMember2021-01-012021-12-310001578732us-gaap:StockAppreciationRightsSARSMember2020-01-012020-12-310001578732mmi:CommissionsPayableMember2022-01-012022-12-310001578732srt:MinimumMembermmi:DeferredCompensationLiabilityMember2022-01-012022-12-310001578732srt:MaximumMembermmi:DeferredCompensationLiabilityMember2022-01-012022-12-310001578732mmi:DeferredCompensationLiabilityMember2022-01-012022-12-310001578732mmi:DeferredCompensationLiabilityMember2021-01-012021-12-310001578732mmi:MarcusAndMillichapCompanyMembermmi:TransitionServicesAgreementMember2022-01-012022-12-310001578732mmi:MarcusAndMillichapCompanyMembermmi:TransitionServicesAgreementMember2021-01-012021-12-310001578732mmi:MarcusAndMillichapCompanyMembermmi:TransitionServicesAgreementMember2020-01-012020-12-310001578732mmi:MarcusAndMillichapCompanyMember2022-01-012022-12-310001578732mmi:MarcusAndMillichapCompanyMember2021-01-012021-12-310001578732mmi:MarcusAndMillichapCompanyMember2020-01-012020-12-310001578732mmi:MarcusAndMillichapCompanyMember2022-12-310001578732mmi:MarcusAndMillichapCompanyMember2021-12-310001578732mmi:ChairmanAndFounderMember2022-01-012022-12-310001578732mmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel1Membermmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel2Membermmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel1Membermmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel2Membermmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:InvestmentsHeldInRabbiTrustMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:MoneyMarketFundsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:MoneyMarketFundsMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2022-12-310001578732us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:LongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:ContingentConsiderationMember2022-12-310001578732us-gaap:FairValueInputsLevel1Membermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732us-gaap:FairValueInputsLevel2Membermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001578732mmi:ContingentConsiderationMemberus-gaap:FairValueInputsLevel3Member2022-12-310001578732mmi:ContingentConsiderationMember2021-12-310001578732us-gaap:FairValueInputsLevel1Membermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732us-gaap:FairValueInputsLevel2Membermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001578732mmi:ContingentConsiderationMemberus-gaap:FairValueInputsLevel3Member2021-12-310001578732srt:MinimumMemberus-gaap:FairValueMeasurementsRecurringMember2022-01-012022-12-310001578732srt:MaximumMemberus-gaap:FairValueMeasurementsRecurringMember2022-01-012022-12-310001578732mmi:ContingentConsiderationMember2020-12-310001578732mmi:ContingentConsiderationMember2022-01-012022-12-310001578732mmi:ContingentConsiderationMember2021-01-012021-12-310001578732mmi:ContingentConsiderationMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ValuationTechniqueDiscountedCashFlowMember2022-12-310001578732us-gaap:MeasurementInputExpectedTermMembersrt:MinimumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-31utr:Y0001578732us-gaap:MeasurementInputExpectedTermMembersrt:MaximumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-310001578732us-gaap:MeasurementInputExpectedTermMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:WeightedAverageMember2022-12-310001578732srt:MinimumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMember2022-12-310001578732srt:MaximumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMember2022-12-310001578732mmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:WeightedAverageMemberus-gaap:MeasurementInputDiscountRateMember2022-12-310001578732mmi:ProbabilityOfAchievementMembersrt:MinimumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-310001578732srt:MaximumMembermmi:ProbabilityOfAchievementMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-310001578732mmi:ProbabilityOfAchievementMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:WeightedAverageMember2022-12-310001578732mmi:ContingentConsiderationMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ValuationTechniqueDiscountedCashFlowMember2021-12-310001578732us-gaap:MeasurementInputExpectedTermMembersrt:MinimumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001578732us-gaap:MeasurementInputExpectedTermMembersrt:MaximumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001578732us-gaap:MeasurementInputExpectedTermMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:WeightedAverageMember2021-12-310001578732srt:MinimumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMember2021-12-310001578732srt:MaximumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMember2021-12-310001578732mmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:WeightedAverageMemberus-gaap:MeasurementInputDiscountRateMember2021-12-310001578732mmi:ProbabilityOfAchievementMembersrt:MinimumMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001578732srt:MaximumMembermmi:ProbabilityOfAchievementMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001578732mmi:ProbabilityOfAchievementMembermmi:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Membersrt:WeightedAverageMember2021-12-3100015787322022-02-162022-02-1600015787322022-08-022022-08-0200015787322022-08-020001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:RestrictedStockMember2022-01-012022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:StockAppreciationRightsSARSMember2022-01-012022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:StockOptionMember2022-01-012022-12-310001578732mmi:PerformanceUnitsMembermmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMember2022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:StockAppreciationRightsSARSMember2022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:StockOptionMember2022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:PerformanceSharesMember2022-01-012022-12-310001578732mmi:PerformanceUnitsMembermmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMember2022-01-012022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMemberus-gaap:PerformanceSharesMember2022-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMembermmi:DeferredStockUnitsMemberMember2022-01-012022-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMember2022-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMember2022-01-012022-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMembermmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMember2022-01-012022-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMembermmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMember2021-01-012021-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMembermmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMember2020-01-012020-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMembermmi:DeferredStockUnitsMemberMember2021-01-012021-12-310001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMembermmi:DeferredStockUnitsMemberMember2020-01-012020-12-310001578732mmi:EmployeeStockPurchasePlanMember2022-12-310001578732mmi:EmployeeStockPurchasePlanAnnualAvailableForIssuanceShareIncreaseMember2022-01-012022-12-310001578732mmi:DeferredStockUnitsMember2013-11-052013-11-050001578732mmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMembermmi:DeferredStockUnitsMember2022-01-012022-12-310001578732mmi:RestrictedStockAndDeferredStockUnitsMembermmi:TwoThousandAndThirteenOmnibusEquityAwardPlanMember2022-01-012022-12-310001578732mmi:EmployeeStockPurchasePlanMember2021-01-012021-12-310001578732mmi:EmployeeStockPurchasePlanMember2020-01-012020-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMember2021-01-012021-12-310001578732mmi:RestrictedStockUnitsAndRestrictedStockAwardsMember2020-01-012020-12-310001578732country:US2022-01-012022-12-310001578732country:US2021-01-012021-12-310001578732country:US2020-01-012020-12-310001578732mmi:ForeignMember2022-01-012022-12-310001578732mmi:ForeignMember2021-01-012021-12-310001578732mmi:ForeignMember2020-01-012020-12-310001578732us-gaap:TaxYear2022Member2022-01-012022-12-310001578732us-gaap:TaxYear2021Member2021-01-012021-12-310001578732mmi:ContributionPlanMember2022-01-012022-12-310001578732us-gaap:ShareBasedCompensationAwardTrancheOneMembermmi:ContributionPlanMember2022-01-012022-12-310001578732mmi:ContributionPlanMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-01-012022-12-310001578732mmi:ContributionPlanMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2022-01-012022-12-310001578732mmi:ContributionPlanMember2021-01-012021-12-310001578732mmi:ContributionPlanMember2020-01-012020-12-310001578732mmi:CreditFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-12-310001578732mmi:CreditFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-07-282022-07-280001578732mmi:CreditFacilityMembersrt:MinimumMembermmi:SecuredOvernightFinancingRateSOFRMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001578732mmi:CreditFacilityMembersrt:MaximumMembermmi:SecuredOvernightFinancingRateSOFRMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001578732mmi:CreditFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001578732mmi:CreditFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-01-012021-12-310001578732mmi:CreditFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2020-01-012020-12-310001578732us-gaap:SubsequentEventMembermmi:MortgageBrokerageBusinessMember2023-01-012023-02-270001578732srt:ScenarioForecastMembermmi:SemiAnnualRegularDividendMember2023-04-060001578732srt:ScenarioForecastMember2023-04-060001578732srt:ScenarioForecastMembermmi:UnvestedRestrictedStockAndDeferredStockUnitsMembermmi:TwoThousandThirteenPlanMember2023-04-060001578732us-gaap:SubsequentEventMember2023-01-012023-02-23

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________

FORM 10-K

________________________

(Mark One)

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022

OR

| | | | | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-36155

________________________

MARCUS & MILLICHAP, INC.

(Exact name of registrant as specified in its charter)

________________________

| | | | | |

| Delaware | 35-2478370 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

23975 Park Sorrento, Suite 400 Calabasas, California, 91302

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (818) 212-2250

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol (s) | | Name of each exchange on which registered |

Common Stock, par value $0.0001 per share | | MMI | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | x | | Accelerated filer | o |

| Non-accelerated filer | o | | Smaller reporting company | o |

| Emerging growth company | o | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the registrant’s voting stock held by non-affiliates at June 30, 2022 was approximately $906.9 million, based on the closing price per share of common stock on June 30, 2022 of $36.74 as reported on the New York Stock Exchange. Shares of common stock known by the registrant to be beneficially owned by directors and executive officers of the registrant and 10% stockholders who are affiliates are not included in the computation. The registrant, however, has made no determination that such persons are “affiliates” within the meaning of Rule 12b-2 under the Securities Exchange Act of 1934.

As of February 23, 2023, there were 39,243,988 shares of the registrant’s common stock outstanding.

________________________

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement to be delivered to stockholders in connection with the annual meeting of stockholders to be held on May 2, 2023 are incorporated by reference into Part III of this Annual Report on Form 10-K. Such Proxy Statement will be filed with the United States Securities and Exchange Commission (the “SEC”) within 120 days of the registrant’s fiscal year ended December 31, 2022.

TABLE OF CONTENTS

MARKET, INDUSTRY AND OTHER DATA

Unless otherwise indicated, information contained in this Annual Report on Form 10-K concerning the commercial real estate industry and the markets in which we operate, including our general expectations and market position, market opportunity and market size, is based on (i) information gathered from various sources, (ii) certain assumptions that we have made, and (iii) on our knowledge of the commercial real estate market. While we believe that the market position, market opportunity and market size information that is included in this Annual Report on Form 10-K is generally reliable,

such information is inherently imprecise. Unless indicated otherwise, the industry data included herein is generally based on information available through the nine months ended September 30, 2022 since full year 2022 information may not yet have been published. We use market data from CoStar Group, Inc. and Real Capital Analytics that consists of list side information of sales transactions of multifamily, retail, office, and industrial buildings, with a value of $1 million or more.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K includes forward-looking statements, including the Company’s business outlook for 2023, the anticipation of further interest rate increases and inflation, the execution of our capital return program, including a semi-annual dividend, and the stock repurchase program, and expectations for market share growth. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting the financial condition of our business. Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily be accurate indications of the times at, or by, which such performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and/or management’s good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

•general uncertainty in the capital markets, a worsening of economic conditions, and the rate and pace of economic recovery following an economic downturn;

•changes in our business operations;

•market trends in the commercial real estate market or the general economy, including the impact of rising inflation and higher interest rates;

•our ability to attract and retain qualified senior executives, managers, and investment sales and financing professionals;

•the effects of increased competition on our business;

•our ability to successfully enter new markets or increase our market share;

•our ability to successfully expand our services and businesses and to manage any such expansions;

•our ability to retain existing clients and develop new clients;

•our ability to keep pace with changes in technology;

•any business interruption or technology failure, including cyber and ransomware attacks, and any related impact on our reputation;

•changes in interest rates, availability of capital, tax laws, employment laws, or other government regulation affecting our business;

•our ability to successfully identify, negotiate, execute, and integrate accretive acquisitions; and

•other risk factors included under “Risk Factors” in this Annual Report on Form 10-K.

In addition, in this Annual Report, the words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “goal,” “expect,” “predict,” “potential,” “should,” and similar expressions, as they relate to our Company, our business, and our management, are intended to identify forward-looking statements. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this Annual Report on Form 10-K may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements.

Forward-looking statements speak only as of the date of this Annual Report on Form 10-K. You should not put undue reliance on any forward-looking statements. We assume no obligation to update forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable laws. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

PART I

Unless the context requires otherwise, the words “Marcus & Millichap,” “MMI,” “we,” the “Company,” “us” and “our” refer to Marcus & Millichap, Inc., and its consolidated subsidiaries.

Item 1. Business

Company Overview

Marcus & Millichap, Inc. (“MMI”) is a leading national real estate services firm specializing in commercial real estate investment sales, financing services, research, and advisory services. We are the leading national investment brokerage company in the $1 million to $10 million private client market segment. This is the largest and most active market segment and comprised approximately 83% of total U.S. commercial property transactions greater than $1 million in the marketplace in 2022. As of December 31, 2022, we had 1,904 investment sales and financing professionals that are primarily exclusive commission-based independent contractors who provide real estate investment brokerage and financing services to sellers and buyers of commercial real estate in 81 offices in the United States and Canada. In 2022, we closed 12,272 sales, financing, and other transactions with total sales volume of approximately $86.3 billion.

We service clients by underwriting, marketing, selling, and financing commercial real estate properties in a manner that maximizes value for sellers, provides buyers with the largest and most diverse inventory of commercial properties, and secures the most competitive financing from lenders for borrowers. Our business model is based on several key attributes:

•for more than 50 years, we have provided investment brokerage and financing services through proprietary inventory and marketing systems, policies and a culture of information sharing, and in-depth investment brokerage training. Our sales force executes these services under the supervision of a dedicated sales management team focused on client service and growing the firm;

•market leading share and brand within the $1 million to $10 million private client market segment, which consistently represents more than 80% of total U.S. commercial property transactions greater than $1 million in the marketplace;

•investment sales and financing professionals providing exclusive client representation across multiple property types;

•a broad geographic platform in the United States and Canada powered by information sharing and proprietary real estate marketing technologies;

•an ability to scale with our private clients as they grow and connect private capital with larger assets through our Institutional Property Advisors (“IPA”) division;

•a financing team integrated with our brokerage sales force providing independent mortgage brokerage services by accessing a wide range of lenders on behalf of our clients;

•a sales management team that supports and leads as Company executives and that does not compete with or participate in investment sales or financing professionals’ commissions; and

•industry-leading research and advisory services tailored to the needs of our clients and supporting our investment sales and financing professionals.

Corporate Information

We were formed as a sole proprietorship in 1971, incorporated in California on August 26, 1976 as G. M. Marcus & Company, and we were renamed as Marcus & Millichap, Inc. in August 1978, Marcus & Millichap Real Estate Investment Brokerage Company in September 1985, and Marcus & Millichap Real Estate Investment Services, Inc., (“MMREIS”), in February 2007. Prior to the completion of our initial public offering (“IPO”), MMREIS was majority-owned by Marcus & Millichap Company (“MMC”) and all of MMREIS’ preferred and common stock outstanding was held by MMC and its affiliates or officers and employees of MMREIS. In June 2013, in preparation for the spin-off of its real estate investment services business, MMC formed a Delaware holding company called Marcus & Millichap, Inc. Prior to the completion of our IPO in November 2013, the shareholders of MMREIS contributed the shares of MMREIS to MMI in exchange for common stock of MMI, and MMREIS became a wholly-owned subsidiary of MMI.

Our Services

We generate revenue by collecting real estate brokerage commissions upon the sale, and financing fees upon the financing of commercial properties, by providing equity advisory services and loan sales, and providing consulting and advisory services. Real estate brokerage commissions are typically based upon the value of the property and financing fees are typically based upon the size of the loan. In 2022, approximately 90% of our revenues were generated from real estate brokerage commissions, 9% from financing fees, and 1% from other revenue, including consulting and advisory services.

We divide commercial real estate into four major market segments, characterized by price in order to understand trends in our revenue from period to period:

•Properties priced less than $1 million;

•Private client market: properties priced from $1 million to up to but less than $10 million;

•Middle market: properties priced from $10 million to up to but less than $20 million; and

•Larger transaction market: properties priced from $20 million and above.

We serve clients with one property, multiple properties and large investment portfolios. The largest group of investors we serve typically transacts in the $1 million to $10 million private client market segment. The investment brokerage and financing professionals serving private clients within the private client market segment represent the largest part of our business, which differentiates us from our competitors. In 2022, approximately 58% of our brokerage commissions came from this market segment. Properties in this market segment are characterized by higher asset turnover rates due to the type of investor as compared to other market segments. Private clients are often motivated to buy, sell and/or refinance properties not only for business reasons but also due to personal circumstances, such as death, divorce, taxes, changes in partnership structures and other personal or financial circumstances. Therefore, private client investors are influenced less by the macroeconomic trends than other large-scale investors, making the private client market segment less volatile over the long-term than other market segments. Accordingly, our business model distinguishes us from our national competitors, who may focus primarily on the more volatile larger transaction and middle market segments, or on other business activities such as leasing or property management, and from our local and regional competitors, who lack a broad national platform.

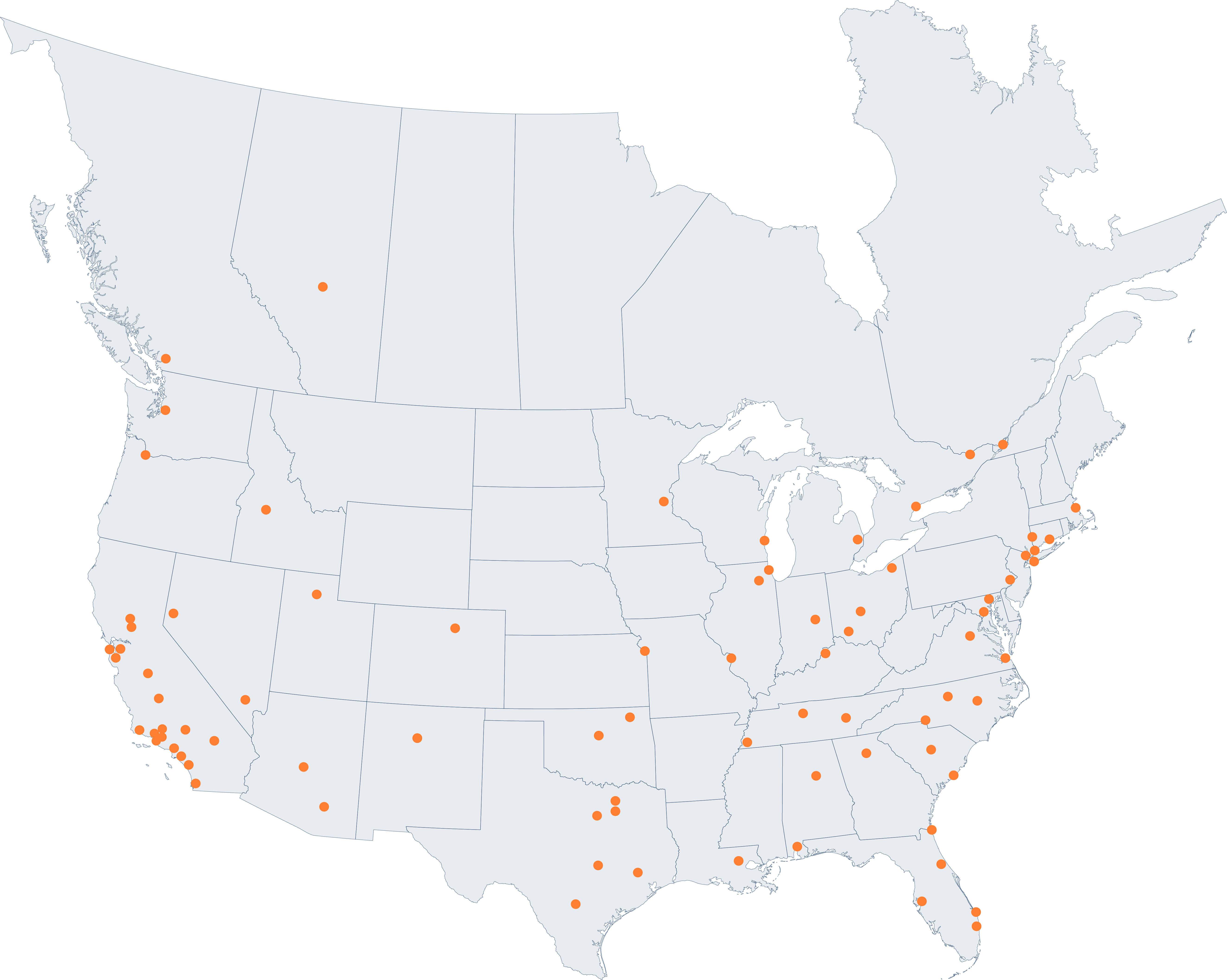

Geographic Locations

We were founded in 1971 in the western United States, and we continue to increase our presence throughout North America through execution of our growth strategies by targeting markets based on population, employment, level of commercial real estate sales, inventory, and competitive landscape opportunities where we believe the markets will benefit from our business model. We have grown to have offices in 36 states across the United States and in four provinces in Canada.

Below is a map reflecting the geographic location of our 81 offices as of December 31, 2022.

Commercial Real Estate Investment Brokerage

Our primary business and source of revenue is the representation of commercial property owners as their exclusive investment broker in the sale of their properties. Our investment sales professionals also represent buyers in fulfilling their investment real estate acquisition needs. Commissions from real estate investment brokerage sales accounted for approximately 90% of our revenue in 2022. Sales are generated by maintaining relationships with property owners, providing market information and trends to them during their investment or “hold” period, and being selected as their representative when they decide to sell, buy additional property, or exchange their property for another property. We collect commissions upon the sale of each property based on a percentage of sales price. These commission percentages are typically inversely correlated with sales price and thus are generally higher for smaller transactions.

We underwrite, value, and market properties to reach the largest and most qualified pool of buyers. We offer our clients one of the industry’s largest team of investment sales professionals, who operate with a culture and policy of information sharing powered by our proprietary system, MNet, which enables real-time buyer-seller matching. We use a proactive marketing campaign that leverages the investor relationships of our entire sales force, direct marketing and a suite of proprietary web-based tools that connects each asset with the right buyer pool. Additionally, in January 2023, we launched a division focused on commercial property auction services to offer clients an accelerated way to buy and sell commercial property as a complement to our traditional property marketing channels. We strive to maximize value for the seller by generating high demand for each property. Our approach also provides a diverse, consistently underwritten inventory of investment real estate for buyers. When a client engages one of our investment sales professionals, they are engaging an entire system, structure, and organization committed to maximizing value for them.

In 2022, we closed 9,111 real estate brokerage transactions in a broad range of commercial property types, with a total sales volume of approximately $68.1 billion. For more than 15 years, we have closed more transactions than any other firm.

We are building on our track record of strength in multifamily, retail, office, and industrial properties by expanding our coverage of additional property types. These include hospitality, self-storage, seniors housing, healthcare, land, and manufactured housing properties, where we are already a leading broker but have significant room for additional growth due to market size, fragmentation, and specific geographic market opportunities. We are also expanding our specialty group management and support infrastructure, specialized branding, and business development customized for each property type. In addition, we are continuously focusing on our recruitment efforts for new and experienced investment sales and financing professionals. We expect that these efforts will expand our presence and result in increased business in these property types.

We service clients in all market segments by underwriting, marketing, selling and financing commercial real estate properties in a manner that maximizes value for sellers and provides buyers with the largest and most diverse inventory of commercial properties. In addition, we achieve growth by leveraging the strength of our relationships in the private client market segment to increase our share of the middle and larger transaction market segments. Because commission rates earned on commercial properties are typically inversely correlated with sales price, our expansion into the middle and larger transaction market segments has led to our average commission rates fluctuating from period-to-period as a result of changes in the relative mix of transactions closed in the middle and larger transaction market segments as compared to the private client market segment.

The following table sets forth the number of investment sales transactions, sales volume, and revenue by commercial real estate market segment for real estate brokerage in 2022 compared to 2021:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2022 | | 2021 | | Change |

| Real Estate Brokerage: | Number | | Volume | | Revenue | | Number | | Volume | | Revenue | | Number | | Volume | | Revenue |

| | | (in millions) | | (in thousands) | | | | (in millions) | | (in thousands) | | | | (in millions) | | (in thousands) |

| <$1 million | 936 | | $ | 560 | | | $ | 24,809 | | | 1087 | | $ | 732 | | | $ | 30,681 | | | (151) | | $ | (172) | | | $ | (5,872) | |

| Private Client Market ($1 – <$10 million) | 6,850 | | 24,474 | | | 682,019 | | | 7,300 | | 24,339 | | | 693,996 | | | (450) | | 135 | | | (11,977) | |

| Middle Market ($10 – <$20 million) | 735 | | 9,980 | | | 188,593 | | | 643 | | 8,874 | | | 170,230 | | | 92 | | 1,106 | | | 18,363 | |

| Larger Transaction Market (≥$20 million) | 590 | | 33,074 | | | 274,889 | | | 622 | | 33,562 | | | 276,062 | | | (32) | | (488) | | | (1,173) | |

| 9,111 | | $ | 68,088 | | | $ | 1,170,310 | | | 9,652 | | $ | 67,507 | | | $ | 1,170,969 | | | (541) | | $ | 581 | | | $ | (659) | |

Financing

Marcus & Millichap Capital Corporation (“MMCC”) is a financial intermediary that provides commercial real estate capital markets solutions, including senior debt, mezzanine debt, joint venture and preferred equity, as well as loan sales and consultative/due diligence services to commercial real estate owners, developers, investors, and capital providers. Our advisors assist clients to secure capital for both acquisitions and the refinancing of single assets and portfolios. MMCC generates revenue from advisory fees collected from capital placement with an assortment of capital providers including national and regional banks, credit unions, private equity funds, insurance companies, government agencies, including the Federal National Mortgage Association (“Fannie Mae”), the Federal Home Loan Mortgage Corporation (“Freddie Mac”), the Federal Housing Administration (“FHA”), conduit lenders, debt funds, hard money lenders, and structured debt facilitators (including preferred equity and mezzanine providers). MMCC additionally receives recurring loan performance fees from certain lenders and other incentive-based fees based on achieving certain production thresholds. MMCC’s financing fees vary by loan amount, transactional complexity, and loan type. In 2022, MMCC completed 2,143 financing transactions representing total financing volume of approximately $12.8 billion, resulting in $113.0 million in financing fees, which accounted for approximately 9% of MMI’s total revenue. The combination of MMCC’s size, market reach, and financing volume enables us to establish long-term relationships with various capital sources. This, in turn, improves MMCC’s value proposition to borrowers who are seeking competitive rates and terms. MMCC seeks to secure the most competitive financing solutions for each client’s specific needs and requirements. During 2022, approximately 41% of MMCC’s revenue came from placing acquisition financing, 37% from refinancing activities, and 22% from other financing activities.

MMCC is fully integrated with the investment sales force in our brokerage offices. MMCC financing professionals are supervised by our MMCC management team and regional managers, who promote cross-selling, information-sharing, business referrals, and high-quality customer service within the offices. The MMCC national network of financing professionals is also supported by a dedicated, nationally focused management team coordinating access to a broad range of national and regional capital sources. By combining these resources with the latest property and capital markets data and information, we can differentiate ourselves in the marketplace and deliver tailored financial solutions that meet our clients’ financial objectives. In 2021, MMCC entered into a strategic alliance with M&T Realty Capital Corporation (“MTRCC”) enabling MMCC to provide clients with increased access to MTRCC’s affordable and conventional multifamily agency financing through a highly streamlined process with dedicated resources. MTRCC has a Delegated Underwriting and Servicing Agreement (“DUS Agreement”) with Fannie Mae and is an approved lender for Freddie Mac’s Conventional and Targeted Affordable Housing loans.

Ancillary Services: Research, Advisory and Consulting

Our research, advisory, and consulting services are designed to assist clients in forming their investment strategy and making transaction decisions. Our advisory and consulting services are coordinated with both our investment sales and financing professionals and are designed to provide market and property focused market research, publications, and customized analysis that increase customer loyalty and help sustain long-term relationships.

We provide a wide range of advisory and consulting services to developers, lenders, owners, real estate investment trusts, high-net-worth individuals, pension fund advisors, and other institutions. Our advisory services include opinions of value, operating and financial performance benchmarking analysis, specific asset buy-sell strategies, market and submarket analysis and ranking, portfolio strategies by property type, market strategy, development and redevelopment feasibility studies, and other services.

Competitive Strengths

We believe the following strengths provide us with a competitive advantage and opportunities for success:

National Platform Built on Investment Brokerage and Financing Services

We have built a leading national platform serving our clients’ needs of investment brokerage and financing services. We continue to be focused on investment brokerage, financing, and other services complementary to our business. Our commitment to specialization is reflected in how we generally organize our investment sales and financing professionals by market area and property type, which enhances our investment sales and financing professionals’ skills, relationships, and market knowledge required for achieving the best results for our clients. As a result of these founding principles, we offer an efficient system of matching each property with the largest pool of qualified buyers and therefore maximizing value in the process.

Market Leader in the Private Client Market Segment

Since our founding, we have focused on being the leading service provider to the $1 million to $10 million private client market segment. This segment is the largest by ownership and transaction count and consistently accounts for over 80% of total U.S. commercial property transactions and over 60% of the commission pool. It is comprised of high-net-worth individuals, partnerships, and small private fund managers with both passive, long-term investments, as well as those with opportunistic and short-term investment horizons. Private clients are often motivated to buy, sell, and/or refinance properties not only for business reasons but also due to personal and financial circumstances. The vast size and personal transaction drivers of private clients make this market segment the most active in terms of sales velocity. In addition, this market segment is highly fragmented with the top 10 brokerage firms accounting for approximately 21% of transactions in 2022. We are the leading broker in the $1 million to $10 million private client market segment based on transaction count in 2022. With our established market leadership and brand name, we have significant room for market share expansion by further consolidating our leadership position in this market segment.

In addition, the private client market segment is characterized by high barriers to entry. These barriers include the need for a large, specialized sales force prospecting private clients, the difficulties in identifying, establishing, and maintaining relationships with such investors, capabilities of exposing properties to a large pool of potential buyers, and the challenge of serving their needs locally, regionally, and nationally. We believe this private client market segment is the

least covered market segment by other national firms and is significantly underserved by local and regional firms that lack a national platform.

Platform Built for Maximizing Investor Value

We have built our business to maximize value for real estate investors through an integrated set of services geared toward our clients’ needs. We are committed to an investment brokerage specialization and providing one of the largest sales force in the industry, promoting a culture and policy of information sharing on each property we represent, and equipping our investment sales professionals with exclusive real estate inventory and marketing technologies that enhance the marketability of the properties we represent. Our system generates real-time buyer-seller matching and maximizes value one property at a time. Our investment sales organization can therefore underwrite and market investment real estate to the largest pool of qualified buyers. We coordinate proactive marketing campaigns across investor relationships and resources of the entire firm, far beyond the capabilities of an individual listing agent. These efforts produce wide exposure to investors whom we identify as high-probability bidders for each property. To grow with our clients, we established the IPA division to serve the needs of our private client investors who are now seeking higher valued properties as well as larger institutional investors. Our ability to bridge private capital with larger, institutional assets creates value for private and larger transaction clients, while offering growth opportunities and strengthening the retention of our investment sales and financing professionals.

We have one of the largest teams of financing professionals in the investment brokerage industry through MMCC. MMCC provides financing expertise and access to debt and capital sources by identifying and securing competitive loan pricing and terms for our clients across a broad range of potential lenders and financing alternatives. Based on the most recent data, we are a leading mortgage broker in the industry based on the number of financing transactions closed in 2022. Our dedicated market research teams analyze the latest local and national economic and real estate trends and produce proprietary analyses for our clients, enabling them to make informed investment and financing decisions. Integrating all these services into a single national platform increases opportunities to maximize value for our clients across multiple property types, market segments, and geographies.

Local Management with Significant Investment Brokerage Experience

Our local management team members are dedicated to recruiting, training, developing, and supporting our investment sales and financing professionals. The majority of our local management team are former senior investment sales professionals of our Company who now focus on management, do not compete with our sales force, and have an average of 14 years of real estate investment brokerage experience with our Company. Our training, development, and mentoring programs rely greatly on the regional managers’ personal involvement. Their past experience as senior investment sales professionals plays a key role in developing new and experienced investment sales and financing professionals. They help our junior professionals establish technical and client service skills as well as set up, develop, and grow relationships with clients. We believe this management structure has helped differentiate the firm from our competitors and ultimately achieves better results for our clients.

Growth Strategy

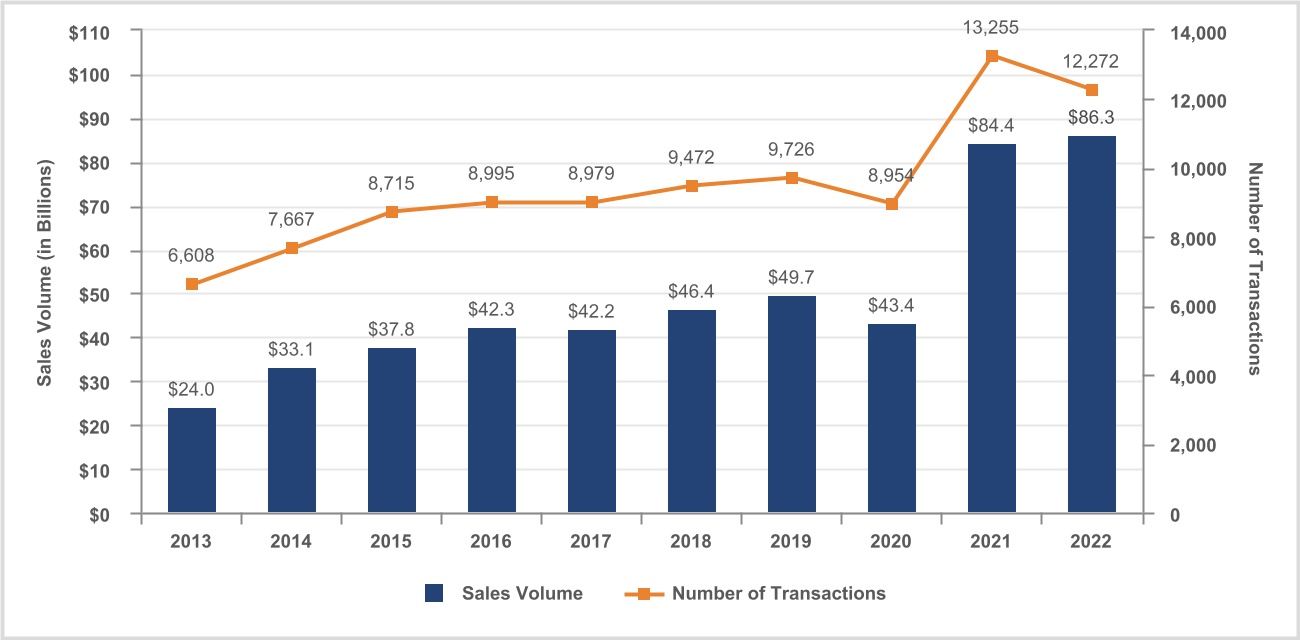

We have demonstrated the ability over the long-term to manage through the cyclical market and continue to be a leader in the $1 million to $10 million private client market segment. The following graph shows the number of transactions and sales volume of all investment sales, financing and other transactions from 2013 to 2022:

We have a long track record of growing our business model driven by opening new offices, recruiting, training, and developing new investment sales and financing professionals as well as deploying our client-focused business model to increase coverage of specialty property types and the middle and larger transaction market segments. Our long-term growth plan has focused on investing in our current business model through organic growth and acquisitions to provide our unique business model to a wider client base. Since 2013, our revenue has increased more than threefold, and we have grown from slightly over 1,000 investment sales and financing professionals to more than 1,900 in the United States and Canada. Our future growth will depend on continually expanding our national footprint and optimizing the size, product segmentation, and specialization of our team of investment sales and financing professionals. The key strategies of our growth plan include:

Increase Market Share in the Private Client Market Segment

Our leading position in the private client market segment and inherent fragmentation continues to provide significant opportunity for us to expand and bring our client service offerings to a larger portion of this expansive market segment. We can continue to leverage our existing platform, relationships, and brand recognition among private clients to grow through expanded marketing and coverage.

Focused Market Expansion

Since we currently have offices in most major-market and mid-market metropolitan cities, our growth is expected to come from focused market expansion in existing office locations and new locations from acquisitions, targeted hiring, and increased coverage of specialty property types. We have targeted markets based on population, employment, level of commercial real estate sales, inventory, and competitive landscape. Our optimal office plans are used to capitalize on these factors by tailoring sales force size, coverage, and composition by office and business activity to direct efforts to offices with the most opportunity where we believe we can leverage our national footprint and proprietary real estate marketing technologies. These initiatives do not require significant increases in the number of offices or in the size of our offices, which allows us to leverage our current office locations without significant incremental investment.

Expand and Develop Our Team of Investment Sales Professionals

A key to growing our business is hiring, training, and developing investment sales professionals. We are always focused on hiring experienced investment sales professionals through our recruiting department, specialty directors, and regional managers in support of our expansion strategy. Our new investment sales professionals are trained in all aspects of real estate fundamentals, client service, and our proprietary marketing technologies through formal training, apprenticeship programs, the William A. Millichap Fellowship Program (discussed below), and mentorship by our dedicated regional, district and division managers, as well as our senior investment sales and financing professionals. As these investment sales professionals mature, we continue to provide them with identified best practices and training in specialty property types. We believe this model creates a high level of teamwork, as well as operational and client service consistency. Please see “Human Capital Management” for more information.

Pursue Selective Acquisitions

Acquisitions continue to be a strategy to supplement the growth of our sales force and the services that we provide to our clients. We continually explore acquisition opportunities to augment our investment brokerage and financing services businesses. We primarily look for acquisitions of small-to-medium size investment brokerage and financing services businesses with teams of professionals with consistent revenue and earnings trends, which will expand our geographic or property type coverage.

Grow in Specialty Property Types and Middle and Larger Transaction Market Segment Presence

Leveraging our current business model into specialty property types and to the middle and larger transaction market segments opens up significant opportunities for growth.

Specialty Property Types

We believe that specialty property types, including hospitality, self-storage, seniors housing, land, and manufactured housing offer significant opportunities for our clients. By deploying our unique business model to increase coverage of these property types, we can create growth for us as well as enhance value for our clients through diversification. To create these opportunities, we are increasing our property type expertise by continuing to strategically add specialty directors who can bring added management capacity, business development, and investment sales professional support. These executives will work with our sales management team to increase investment sales professional hiring, training, development, and redeployment and to execute various branding and marketing campaigns to expand our presence in these targeted property types.

Middle and Larger Transaction Market Segments Presence

Our extensive relationships with private client investors who typically invest in the $1 million to $10 million private client market segment have enabled us to capture a greater portion of commercial real estate transactions in excess of $10 million and bridge the private client market investor to the middle market and larger transaction market segments in recent years. As property values increase and investors grow and expand, they require larger properties. Our IPA division positions us to provide our unique investment brokerage and financing services to investors in those market segments. Our ability to connect private client capital with middle and larger transaction market segment properties allows us to continue to serve our clients as they grow and plays a major role in differentiating our services. The IPA division is a group dedicated to servicing larger investors. This strategy has had market acceptance and provides a vehicle for growth by delivering our unique service platform within the middle and larger transaction market segments for the multifamily, retail, and office property types. The evolution of our investors and their utilization of our IPA division has driven incremental growth in these market segments. Hiring multiple investment sales teams into IPA in 2022 has expanded our capability to service clients and furthers our growth plan.

Expand Marcus & Millichap Capital Corporation Financing Business

Our growth plan for MMCC continues to focus on expanding our capital markets services in markets currently served by our investment sales brokerage offices and other strategic markets. This includes increasing the capacity of the existing professionals in offices we currently serve and integrating financing professionals and related services in offices that do not have an MMCC presence. We will also continue to expand our service platform by increasing access to a broad array of new capital resources and pursuing selective acquisitions. We have and continue to expand MMCC’s capital markets advisory services and added complementary services in loan sales, consultative/due diligence, and debt and equity

advising through acquisitions, as well as expanded service offerings. While maintaining a core focus on our private client segment, MMCC, through the IPA division, has commenced a focus on institutional clients. These specialized financing professionals work closely with IPA investment sales professionals across the country, supporting them and their clients in their financing needs as well as working directly with institutional clients.

We have established alliances with national capital sources that provide access to an assortment of highly competitive products including Fannie Mae, Freddie Mac, and FHA. These alliances serve to expand the distribution network for each of our capital partners, while affording our financing professionals and clients with more favorable pricing and terms. We will continue to hire and acquire experienced financing professionals and companies to further grow our MMCC business, support the growth of our service platform, and establish relationships with various capital sources. Further, our internally developed training programs are directed at enhancing the skill sets for our professionals, promoting the MMCC value proposition, increasing our internal capture rate with our investment sales brokerage clients, and increasing activity with non-brokerage clients. As of December 31, 2022, we had 34 offices with financing professionals. We continue to capitalize on the synergies our financing professionals provide to our client-focused service platform with financing fees increasing 3.0% from $109.7 million in 2021 to $113.0 million in 2022.

Seasonality

There is seasonality in our real estate brokerage commissions and financing fees, which has generally caused our revenue, operating income, net income, and cash flows from operating activities to be lower in the first half of the year and higher in the second half of the year, particularly in the fourth quarter. This historical trend could be disrupted either positively or negatively by market trends, macroeconomic uncertainties, geopolitical events, or natural disasters, which may impact, among other things, investor sentiment for a particular property type or location, volatility in financial markets, current and future projections of interest rates, attractiveness of other asset classes, market liquidity, and the extent of limitations or availability of capital allocations for larger property buyers. For a more detailed description of our seasonality, refer to Item 1A – “Risk Factors – External Business Risks – Seasonal fluctuations and other market data in the investment real estate industry could adversely affect our business and make comparisons of our quarterly results difficult” and Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview – Seasonality” of this Annual Report on Form 10-K.

Competition