UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-36155

MARCUS & MILLICHAP, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 35-2478370 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

23975 Park Sorrento, Suite 400 Calabasas, California, 91302

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (818) 212-2250

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.0001 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the registrant’s voting stock held by non-affiliates at June 30, 2015 was approximately $651.9 million, based on the closing price per share of common stock on that date of $46.14 as reported on the New York Stock Exchange. Shares of common stock known by the registrant to be beneficially owned by directors and executive officers of the registrant and 10% stockholders are not included in the computation. The registrant, however, has made no determination that such persons are “affiliates” within the meaning of Rule 12b-2 under the Securities Exchange Act of 1934.

As of March 2, 2016, there were 37,568,389 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement to be delivered to stockholders in connection with the annual meeting of stockholders to be held on May 3, 2016 are incorporated by reference into Part III of this Annual Report on Form 10-K. Such Proxy Statement will be filed with the United States Securities and Exchange Commission (the “SEC”) within 120 days of the registrant’s fiscal year ended December 31, 2015.

MARKET, INDUSTRY AND OTHER DATA

Unless otherwise indicated, information contained in this Annual Report on Form 10-K concerning the commercial real estate industry and the markets in which we operate, including our general expectations and market position, market opportunity and market size, is based on (i) information gathered from various sources, (ii) certain assumptions that we have made, and (iii) on our knowledge of the commercial real estate market. While we believe our market position, market opportunity and market size information included in this Annual Report on Form 10-K are generally reliable, such information is inherently imprecise. Unless indicated otherwise, the industry data included herein is generally based on information available through the nine months ended September 30, 2015 since full year 2015 information may not yet have been published. We use market data from Costar Group, Inc. and Real Capital Analytics that consists of list side information of sales transactions, with a value of $1 million or more, of multifamily, retail, office and industrial buildings.

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K includes forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting the financial condition of our business. Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time those statements are made and/or management’s good faith belief as of that time with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

| • | market trends in the commercial real estate market or the general economy; |

| • | our ability to attract and retain qualified managers, investment sales and financing professionals; |

| • | the effects of increased competition on our business; |

| • | our ability to successfully enter new markets or increase our market share; |

| • | our ability to successfully expand our services and businesses and to manage any such expansions; |

| • | our ability to retain existing clients and develop new clients; |

| • | our ability to keep pace with changes in technology; |

| • | any business interruption or technology failure and any related impact on our reputation; |

| • | changes in tax laws, employment laws or other government regulation affecting our business; and |

| • | other risk factors included under “Risk Factors” in this Annual Report on Form 10-K. |

In addition, in this Annual Report, the words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “predict,” “potential” and similar expressions, as they relate to our company, our business and our management, are intended to identify forward-looking statements. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this Annual Report on Form 10-K may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements.

Forward-looking statements speak only as of the date of this Annual Report on Form 10-K. You should not put undue reliance on any forward-looking statements. We assume no obligation to update forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable laws. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

3

Unless the context requires otherwise, the words “Marcus & Millichap,” “Marcus & Millichap Real Estate Investment Services,” “MMREIS,” “we,” the “Company,” “us” and “our” refer to Marcus & Millichap, Inc., Marcus & Millichap Real Estate Investment Services, Inc. and its other consolidated subsidiaries.

Overview

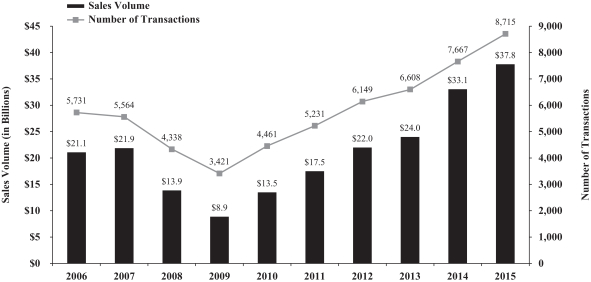

Marcus & Millichap, Inc. (“MMI”) is a leading national brokerage firm specializing in commercial real estate investment sales, financing, research and advisory services. We have been the top broker in the United States based on the number of investment transactions over the last 10 years. As of December 31, 2015, we had over 1,600 investment sales and financing professionals in 79 offices in the United States and Canada that provide investment brokerage and financing services to sellers and buyers of commercial real estate. In 2015, we closed 8,715 sales, financing and other transactions with total sales volume of approximately $37.8 billion.

We divide commercial real estate into four major market segments, characterized by price:

| • | Properties with prices less than $1 million; |

| • | Private client market: properties priced from $1 million up to $10 million; |

| • | Middle market: properties priced from $10 million up to $20 million; and |

| • | Institutional market: properties priced from $20 million and above. |

We service clients in all of these market segments by underwriting, marketing and selling commercial real estate properties in a manner that maximizes value for sellers and provides buyers with the largest and most diverse inventory of commercial properties. Our business model is based on several key attributes:

| • | a 45-year history of providing investment brokerage and financing services through a proprietary marketing system, policies and culture of information sharing and in-depth investment brokerage training, all of which is executed under the supervision of a dedicated management team focused on client service and growing the firm; |

| • | market leading share and brand within the $1-$10 million private client market segment, which consistently represents more than 80% of commercial property sales greater than $1 million in the marketplace; |

| • | Over 1,600 investment sales and financing professionals providing consistent services and exclusive client representation across multiple property types; |

| • | a broad geographic platform consisting of 79 offices in the United States and Canada powered by information sharing and proprietary real estate marketing technologies; |

| • | an ability to scale with our private clients as they grow and connect private capital with larger, institutional assets through our Institutional Property Advisors (“IPA”) group; |

| • | a financing team integrated with our brokerage salesforce providing independent mortgage brokerage services; |

| • | an experienced management team overseeing our offices, with an average of approximately 10 years of real estate investment brokerage experience with our Company; our managers do not compete with or participate in sales professionals commissions; they are in a support and leadership role as company executives; and |

| • | industry-leading research and advisory services tailored to the needs of our clients and supporting our investment sales and financing professionals. |

4

The investment brokerage and financing businesses serving private clients within the $1-$10 million private client market segment represent the largest part of our business which differentiates us from our competitors. In 2015, approximately 69% of our brokerage commissions came from this segment. Accordingly, our business model distinguishes us from our national competitors, who may focus primarily on the more volatile institutional market segment or on other business activities such as leasing or property management, and from our local and regional competitors, who lack a broad national platform.

Our business model and geographic footprint provide an unparalleled level of connectivity to the marketplace for our clients. Our investment sales and financing professionals are specialized by property type and by local market area, as we believe this focused expertise brings value to our clients. Our broad geographic coverage, encompassing 79 offices in the United States and Canada, combined with our local and national property expertise and significant relationships with both buyers and sellers, provides exposure and access to properties across the United States and Canada. This connectivity to a broad marketplace increases liquidity and opportunities for our clients as we maximize the value of their properties by accessing the largest pool of qualified buyers through our network of sales professionals and proprietary real estate marketing system. By closing more transactions annually than any other brokerage firm, our investment sales professionals are able to provide clients with a broad and deep perspective in multiple property types in real estate markets locally, regionally and nationally.

Our experienced management team is responsible for developing and mentoring our investment sales and financing professionals creating a consistent culture of information sharing and environment of best practices to maximize value for our clients. Our managers are compensated as executives incentivized to grow their offices and do not participate in commissions generated by our sales and financing professionals. This structure eliminates any competition with our salesforce and puts the emphasis on sales and financing professionals’ support and client service. In addition, we support our clients and investment sales and financing teams with market and property focused research, publications and custom analysis.

We generate revenues by collecting fees upon the sale and financing of commercial properties. These fees consist of commissions collected upon the sale of a property and fees collected from the placement of loans. The fees are principally based upon the sales price of the property or amount financed. In 2015, approximately 92% of our revenues were generated from real estate brokerage commissions, 6% from financing fees and 2% from other revenues, including consulting and advisory services. In 2015, 69% of our real estate brokerage commissions were generated from the $1-$10 million private client market segment.

Corporate Information

We were formed as a sole proprietorship in 1971, incorporated in California on August 26, 1976 as G. M. Marcus & Company, and we were renamed as Marcus & Millichap, Inc. in August 1978, Marcus & Millichap Real Estate Investment Brokerage Company in September 1985, and Marcus & Millichap Real Estate Investment Services, Inc. (“MMREIS”) in February 2007. Prior to the completion of our initial public offering (“IPO”), MMREIS was majority-owned by Marcus & Millichap Company (“MMC”) and all of MMREIS’ preferred and common stock outstanding was held by MMC and its affiliates or officers and employees of MMREIS. In June 2013, in preparation for the spin-off of its real estate investment services business (the “Spin-Off”), MMC formed a holding company called Marcus & Millichap, Inc. in Delaware. Prior to the completion of our IPO, the shareholders of MMREIS contributed the shares of MMREIS to Marcus & Millichap, Inc. in exchange for common stock of Marcus & Millichap, Inc., and MMREIS became a wholly owned subsidiary of Marcus & Millichap, Inc. On November 5, 2013, MMI completed its IPO.

Our principal executive offices are located at 23975 Park Sorrento, Suite 400 Calabasas, California 91302. Our telephone number at this location is (818) 212-2250. Our website address is www.marcusmillichap.com. The information on our website is not part of, and is not incorporated into, this Annual Report on Form 10-K.

5

Competitive Strengths

We believe the following strengths provide us with a competitive advantage and opportunities for success:

National Platform Built on Investment Brokerage and Financing Services

We have built a leading national platform serving our clients’ needs of investment brokerage and financing services. We continue to be focused on investment brokerage and financing services as opposed to other businesses such as leasing or property management. We equip our highly qualified investment sales and financing professionals in 79 offices across the United States and Canada with proprietary real estate marketing technologies and processes to market investment real estate for our clients. Our commitment to specialization is reflected in how we generally organize our investment sales and financing professionals by market area and property type, which enhances our investment sales and financing professionals’ skills, relationships and market knowledge required for achieving the best results for our clients. As a result of these founding principles, we offer an efficient system of matching every property with the largest pool of qualified buyers and maximize value in the process.

Market Leader in the Private Client Market Segment

Since our founding in 1971, we have focused on being the leading service provider to the $1-$10 million private client market segment. This segment is the largest by ownership and transaction count, which consistently accounts for over 80% of commercial property sales. It is comprised of high-net-worth individuals, partnerships and small private fund managers with both passive, long-term investments as well opportunistic, short-term investment horizons. Private clients are often motivated to buy, sell and/or refinance properties due to personal circumstances such as death, divorce, partnership breakups and estate planning in addition to macroeconomic and capital market trends and events. The vast size and personal transaction drivers of private clients make this market segment the most active in terms of sales velocity. Therefore, sales in the private client market segment tend to be less volatile than higher priced properties priced at $10 million and above over the long term. In addition, this market segment is highly fragmented with the top ten brokerage firms accounting for 24% of transactions in 2015. Marcus & Millichap is the leading broker in the $1-$10 million private client market segment with an 8% market share by transaction count. With our established market leadership and our brand name, Marcus & Millichap has significant room for market share expansion by further consolidating its leadership position in this market segment.

In addition, the private client market segment is characterized by high barriers to entry. These barriers include the need for a large specialized salesforce prospecting private clients, difficulties in identifying, establishing and maintaining relationships with such investors, capabilities of exposing properties to a large pool of potential buyers and the challenge of serving their needs locally, regionally and nationally. We believe this private client market segment is the least covered market segment by other national firms and is significantly underserved by local and regional firms that lack a multi-market platform.

Platform Built for Maximizing Investor Value

We have built our business to maximize value for real estate investors through an integrated set of services geared toward our clients’ needs. We are committed to an investment brokerage specialization, provide one of the largest salesforce in the industry, a culture and policy of information sharing on each property we represent and equip our investment sales professionals with proprietary real estate marketing technologies that enhance the marketability of the properties we represent. Our system generates real-time buyer-seller matching and maximizes value one property at a time. Our investment sales organization can therefore underwrite, position and market investment real estate to the largest pool of qualified buyers. We coordinate proactive marketing campaigns across investor relationships and resources of the entire firm, far beyond the capabilities of an individual listing agent. These efforts produce wide exposure to investors who we identify as high-probability

6

bidders for each property. To grow with our clients, we established the IPA group to serve the needs of our private client investors that are now seeking higher valued properties as well as larger institutional investors. Our ability to bridge private capital with larger, institutional assets creates value for private and institutional clients while strengthening the retention of our sales and financing professionals.

We have one of the largest teams of financing professionals in the investment brokerage industry through Marcus & Millichap Capital Corporation (“MMCC”). MMCC provides financing expertise and access to debt and capital sources by identifying and securing competitive loan pricing and terms for our clients across a broad range of potential lenders and financing alternatives. We are a leading mortgage broker in the industry based on the number of financing and loan value transactions closed in 2015. Finally, our dedicated market research teams analyze the latest local and national economic and real estate trends and produce proprietary analyses for our clients enabling them to make informed investment and financing decisions. Our research team produces more than 900 reports, publications and briefs addressing real estate investment trends. Integrating all these services into one national platform increases opportunities to maximize value for our clients across multiple property types, market segments and geographies.

Management with Significant Investment Brokerage Experience

Our management team, as executives of the firm, is dedicated to recruiting, training, developing and supporting our investment sales and financing professionals. The majority of our management team are former senior sales professionals of our Company who now focus on management, do not compete with our salesforce and have an average of approximately 10 years of real estate investment brokerage experience with our Company. Our training, development and mentoring programs rely greatly on the regional managers’ personal involvement. Their past experience as senior investment sales professionals plays a key role in developing new and experienced investment sales and financing professionals. They help our junior professionals establish technical and client service skills as well as setting up, developing and growing relationships with clients. We believe this management structure has helped differentiate the firm from our competitors and ultimately achieve better results for our clients.

Growth Strategy

We have a long track record of growing our business model driven by opening new offices, recruiting, training and developing new investment sales and financing professionals as well as deploying our client-focused business model to increase coverage of specialty property types and the middle and institutional market segments. Our long-term growth plan has focused on investing in our current business model through growing internally and by providing our unique business model to a wider client base. Since 2010, our revenue has increased threefold and we have grown from 1,066 investment sales and financing professionals to over 1,600 investment sales and financing professionals in the United States and Canada. Our future growth will depend on continually expanding our national footprint and optimizing the size, product segmentation and specialization of our team of investment sales and financing professionals. The key strategies of our growth plan include:

Increase Market Share in the Private Client Market Segment

The $1-$10 million private client market segment is fragmented and underserved. The top 10 brokerage firms accounted for only approximately 24% of 2015 transactions in this market segment. Our industry leading market share in this segment increased to 8.0% in 2015 from approximately 6.9% in 2012. Our leading position in this market segment and inherent fragmentation continues to provide significant opportunity for us to expand and bring our client service offerings to a larger portion of this expansive market segment. We can continue to leverage our existing platform, relationships and brand recognition among private clients to grow through expanded marketing and coverage.

7

Focused Office Expansion

Since we currently have offices in most major-market and mid-market metropolitan cities, our growth is expected to come from focused office expansion, targeted hiring and increased coverage of specialty property types. We have targeted markets based on population, employment, level of commercial real estate sales, inventory and competitive landscape. Our optimal office plans are used to capitalize on these factors by tailoring salesforce size, coverage and composition by office and business activity to direct resources to offices with the most opportunity where we believe we can leverage our national footprint and proprietary real estate marketing technologies. These initiatives do not require a significant increase in the number of offices or significant increase in the size of our offices, which allows us to leverage our current office locations without significant incremental investment.

Expand and Develop Our Team of Investment Sales Professionals

A key to growing our business is hiring, training and developing investment sales professionals. We have increased our focus on hiring experienced investment sales professionals through our recruiting department, specialty directors and regional managers in support of our optimal office plans. Our new investment sales professionals are trained in all aspects of real estate fundamentals, client service and proprietary marketing technologies through formal training, apprenticeship programs and mentorship by our non-competitive and dedicated regional managers. As these investment sales professionals mature, we continue to provide them with identified best practices and training in specialty property types. We believe this model creates a high level of teamwork, as well as operational and client service consistency. During 2015, we reached an all-time high in the number of investment sales professionals, ending the year with over 1,500.

Grow in Specialty Property Types and Middle and Institutional Market Segment Presence

Leveraging our current business model into specialty property types and to the middle and institutional market segments opens up significant opportunities for growth.

Specialty Property Types

We believe that specialty property types, including hospitality, self-storage, seniors housing, land and manufactured housing offer significant opportunities for our clients. By deploying our unique business model to increase coverage of these property types, we can create growth for us as well as enhance value for our clients through diversification. To create these opportunities, we are increasing our property type expertise by continuing to add specialty directors who can bring added management capacity, business development and sales professional support. These executives will work with our regional and group managers to increase sales professional hiring, training, development and redeployment and to execute various branding and marketing campaigns to expand our presence in these targeted property types. The number and volume of transactions in the core property types of multifamily, retail, office and industrial should continue to grow with upside opportunity, particularly in the office and industrial properties. At the same time, we intend to continue to grow our presence in specialty property types, which registered growth in number of transactions of 26% and volume of 36% in 2015 compared to 2014.

Middle and Institutional Market Segments Presence

Our extensive relationships with private investor clients who typically invest in the $1-$10 million private client market segment have enabled us to capture a greater portion of commercial real estate transactions in excess of $10 million and bridge the private client market investor to the middle market and institutional market segments in recent years. As property values increase and investors grow and expand, they require larger properties and we are organized to provide our unique brokerage and financing services to them in those market segments. Our ability to connect historically private client capital with middle and institutional market segment

8

properties allows us to continue to serve our clients as they grow and plays a major role in differentiating our services. In 2011, we introduced a group dedicated to serving major investors branded as Institutional Property Advisors, specifically to service larger multifamily investors. This strategy has met with great success and market acceptance and provides a vehicle for growth by delivering our unique service platform within the middle and institutional multifamily, retail and office property types. The growth of our investors and introduction of IPA has driven incremental growth for us. Brokerage commissions from the middle and institutional market segments have grown approximately 17% to $163.4 million in 2015 from $139.9 million in 2014.

Expand Marcus & Millichap Capital Corporation Financing Business

We are dedicated to growing our financing services through our MMCC platform. Our focus continues to be expanding financing services in markets currently served by our investment brokerage offices, increasing the capacity of financing professionals in offices we currently serve, integrating financing professionals in offices that do not have an MMCC presence and expanding our service platform by creating access to other capital resources such as mezzanine financing, HUD products, equity placement and conduit financing. Our internally developed training programs are directed to enhancing our internal branding, skill development, increasing our internal capture rate and cross-selling with a focus on the MMCC value proposition for our brokerage and non-brokerage clients. We will continue to seek out and hire experienced financing professionals and capital markets teams to grow our MMCC business to support the growth in our service platform and establish relationships with various capital sources. We have grown the number of financing professionals to 98 in 2015 from 82 in 2014. As of December 31, 2015, we have 40 offices with financing professionals embedded with our brokerage teams. We continue to capitalize on the synergies our financing professionals provide to our client focused service platform with approximately 26% growth in financing fees to $42.6 million in 2015 from $33.9 million in 2014.

Our Company

We provide investment brokerage and financing services to investors of all sizes and types of commercial real estate properties. We are a leading national investment brokerage company in the $1-$10 million private client market segment. This is the largest and most active market segment and comprised approximately 83% of total U.S. commercial property sales in 2015. We have over 1,600 investment sales and financing professionals in 79 offices in the United States and Canada. We have 60 offices concentrated in 48 major markets consisting of metropolitan areas with a population of at least 1 million and 19 offices in 19 mid-market locations consisting of metropolitan areas with a population of less than 1 million. We leverage our relationships with investors and use proprietary marketing tools to match properties with qualified buyers. Our financing professionals obtain competitive debt financing for buyers of our properties and owners who need to refinance or restructure their positions.

We have a 45 year history in the real estate marketplace. The real estate market is cyclical, and our results are impacted by many macro and microeconomic factors as discussed in Item 1A – Risk Factors. We have demonstrated the ability, over the long term, to manage through the cyclical market and continue to be a leader in the $1-10 million private client market segment. The most recent downturn began in 2007 when the global credit markets began to show signs of distress resulting in a shortage of liquidity in some financing markets, including real estate. Beginning in late 2008, the credit crisis and recession greatly affected the commercial real estate industry, resulting in a dramatic decline in sales volume and revenue. Despite the severity of the market downturn, we maintained all of our offices and services, enabling us to quickly take advantage of the market recovery and resume our growth. As the real estate and financing markets recovered after 2009, our sales volume has steadily grown and now exceeds pre-downturn levels both as a result of the market transaction growth and

9

executing our growth initiatives which expanded our market presence. The following graph shows the number of transactions and sales volume of investment sales, financing and other transactions from 2006 to 2015:

Geographic Locations

We have grown to have offices in 34 states across the United States and in three provinces in Canada, with over 1,600 investment sales and financing professionals in 60 offices in major metropolitan markets and 19 offices in mid-market locations. Below is a map reflecting the geographic location of our offices as of December 31, 2015.

10

Geographic Concentrations

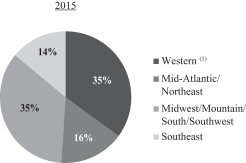

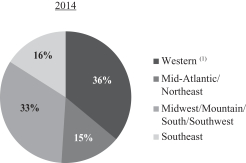

We were founded in 1971 in the western United States, and we continue to increase our presence in states in the Mid-Atlantic, Northeast, Midwest, Mountain and the South regions through execution of our growth strategies by targeting markets based on population, employment, level of commercial real estate sales, inventory and competitive landscape opportunities where we believe the markets will benefit from our business model. The following charts set forth the percentage of transactions by region for our investment sales transactions in 2015 and 2014.

|

|

| (1) | Includes our Canadian operations, which represented less than 1.0% of our total revenues in each period presented. |

Commercial Real Estate Market Segments

We divide the commercial real estate market into four major market segments, characterized by investment size. Our strength is in serving private clients in the $1-$10 million private client market segment, which contributed approximately 69% of our brokerage commissions in 2015. In addition, we achieved growth by leveraging the strength of our relationships in the private client market segment to increase our share of the middle and institutional market segments. Commission percentages are generally lower in the middle and institutional market segments since commission rates earned on commercial properties are typically inversely correlated with sales price. As a result of the expansion into the middle and institutional market segments, we have seen our average commission rates fluctuate from period-to-period as a result of changes in the relative mix of transactions closed in the middle and institutional market segments as compared to the private client market segment.

The following table sets forth the number of transactions, sales volume and revenue by commercial real estate market segment for real estate brokerage in 2015 compared to 2014:

| 2015 | 2014 | Change | ||||||||||||||||||||||||||||||||||

| Real Estate Brokerage: |

Number | Volume | Revenues | Number | Volume | Revenues | Number | Volume | Revenues | |||||||||||||||||||||||||||

| (in millions) | (in thousands) | (in millions) | (in thousands) | (in millions) | (in thousands) | |||||||||||||||||||||||||||||||

| <$1 million |

1,174 | $ | 718 | $ | 29,971 | 1,300 | $ | 792 | $ | 33,931 | (126 | ) | $ | (74 | ) | $ | (3,960 | ) | ||||||||||||||||||

| Private Client Market ($1-$10 million) |

4,611 | 14,898 | 439,164 | 3,825 | 11,748 | 351,135 | 786 | 3,150 | 88,029 | |||||||||||||||||||||||||||

| Middle Market (³$10-$20 million) |

352 | 4,776 | 89,886 | 306 | 4,184 | 78,067 | 46 | 592 | 11,819 | |||||||||||||||||||||||||||

| Institutional Market (³$20 million) |

195 | 8,052 | 73,553 | 157 | 8,627 | 61,818 | 38 | (575 | ) | 11,375 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| 6,332 | $ | 28,444 | $ | 632,574 | 5,588 | $ | 25,351 | $ | 524,951 | 744 | $ | 3,093 | $ | 107,623 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

11

Property Type

We have a long history and significant expertise in our core property types of multifamily, retail, office and industrial. We have expanded our expertise in the specialty property types by hiring and assigning specialty directors to coordinate our national presence in these property types and expand our market share.

The following table sets forth the number and sales volume (dollars in billions) of investment sales, financing and other transactions in 2015 compared to 2014 by property type:

| 2015 | 2014 | Change | ||||||||||||||||||||||

| Number | Volume | Number | Volume | Number | Volume | |||||||||||||||||||

| Core Property Types: |

||||||||||||||||||||||||

| Multifamily |

3,382 | $ | 17.9 | 3,142 | $ | 16.1 | 240 | $ | 1.8 | |||||||||||||||

| Retail |

3,351 | 10.8 | 2,948 | 10.3 | 403 | 0.5 | ||||||||||||||||||

| Office |

567 | 2.4 | 480 | 1.8 | 87 | 0.6 | ||||||||||||||||||

| Industrial |

253 | 1.0 | 172 | 0.7 | 81 | 0.3 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Core Property Types |

7,553 | $ | 32.1 | 6,742 | $ | 28.9 | 811 | $ | 3.2 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Specialty Property Types: |

||||||||||||||||||||||||

| Hospitality |

225 | 1.6 | 240 | 1.1 | (15 | ) | 0.5 | |||||||||||||||||

| Self-Storage |

201 | 0.9 | 160 | 0.7 | 41 | 0.2 | ||||||||||||||||||

| Seniors Housing |

83 | 0.9 | 61 | 0.7 | 22 | 0.2 | ||||||||||||||||||

| Land |

266 | 0.6 | 173 | 0.5 | 93 | 0.1 | ||||||||||||||||||

| Manufactured Housing |

101 | 0.4 | 90 | 0.4 | 11 | — | ||||||||||||||||||

| Mixed – Use / Other |

286 | 1.3 | 201 | 0.8 | 85 | 0.5 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Specialty Property Types |

1,162 | $ | 5.7 | 925 | $ | 4.2 | 237 | $ | 1.5 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| 8,715 | $ | 37.8 | 7,667 | $ | 33.1 | 1,048 | $ | 4.7 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Our Services

We serve clients with one property, multiple properties and large investment portfolios. The largest group of investors we serve typically transacts in the $1-$10 million private client market segment. Properties in this market segment are characterized by higher asset turnover rates due to the type of investor as compared to other market segments. Investors in the private client market segment typically transact due to personal circumstances and business reasons, such as death, divorce, changes in partnership structures and other personal or financial circumstances. Therefore private client investors are influenced less by the macroeconomic trends than other large scale investors making the private client market segment less volatile over the long term than other market segments. We offer two primary services to our clients, commercial real estate investment brokerage and financing and ancillary services including other research, advisory and consulting services.

Commercial Real Estate Investment Brokerage

Our primary business and source of revenue is the representation of commercial property owners as their exclusive investment broker in the sale of their properties. Commissions from real estate investment brokerage sales accounted for approximately 92% of our revenues in 2015. Sales are generated by maintaining relationships with property owners, providing market information and trends to them during their investment or “hold” period and being selected as their representative when they decide to sell, buy additional property or exchange their property for another property. We collect commissions upon the sale of each property based on a percentage of sales price. These commission percentages are typically inversely correlated with sales price and thus are generally higher for smaller transactions. Our investment sales professionals also represent buyers in fulfilling their investment real estate acquisition needs; however, the vast majority of our investment sales business is generated from our exclusive representation of sellers.

12

We underwrite, value, position and market properties to reach the largest and most qualified pool of buyers. We offer our clients the industry’s largest team of investment sales professionals operating with a culture and policy of information sharing, powered by our proprietary system, MNet, which enables real-time buyer-seller matching. We use a proactive marketing campaign that leverages the investor relationships of our entire salesforce, direct marketing and a suite of proprietary web-based tools that connects each asset with the right buyer pool. We strive to maximize value for the seller by generating high demand for each property. Our approach also provides a diverse, consistently underwritten inventory of investment real estate for buyers. When a client engages one of our investment sales professionals, they are engaging an entire system, structure and organization committed to maximizing value for them.

In 2015, we closed 6,332 real estate brokerage transactions in a broad range of commercial property types, with a total sales volume of approximately $28.4 billion. In the last 10 years, we have closed more transactions than any other firm. We have significantly diversified our business beyond our historical focus on multifamily properties.

The majority of our business activity is in the $1-$10 million private client market segment and is aligned with the largest real estate market segment. During 2015, we closed 4,611 real estate brokerage transactions in this segment, which comprised approximately 89% of our total real estate brokerage transactions greater than $1 million and 73% of our brokerage commissions for transactions greater than $1 million. Of the commercial real estate industry as a whole, the $1-$10 million private client market segment represented over 80% of total transactions greater than $1 million in 2015.

We are building on our track record of growth in multifamily, retail, office and industrial by expanding our coverage of additional property types. These include hospitality, self-storage, seniors housing, land and manufactured housing, where we are already a leading broker but have significant room for additional growth due to market size, fragmentation and specific geographic market opportunities. We are also expanding our specialty group management and support infrastructure, specialized branding and business development customized for each property type and intensifying our recruiting efforts, for management and investment sales and financing professionals. These efforts should expand our presence and result in increased business in these property types.

Financing

MMCC is a broker of debt financing for commercial properties principally in the under $10 million market segments. We generate revenue in the form of financing fees collected from the placement of loans with banks, insurance companies, government agencies, commercial mortgage backed securities (“CMBS”) and conduits. MMCC’s financing fees vary by loan amount and type. In 2015, MMCC completed more than 1,600 financing transactions with a sales volume of approximately $4.9 billion and accounted for approximately 6% of our revenues. MMCC’s size, market reach and sales volume enables us to establish long-term relationships and special programs with various capital sources. This in turn improves MMCC’s value proposition to borrowers seeking competitive financing rates and terms. MMCC is not limited to promoting in-house or exclusive capital sources and seeks the most competitive financing solution for each client’s specific needs and circumstances. We place loans for refinancing as well as acquisition financing for individual assets and portfolios. During 2015, approximately 49% of MMCC’s revenues came from placing acquisition financing, 47% from refinance activities and 4% from other financing activities.

MMCC is fully integrated with our investment salesforce in our brokerage offices. MMCC financing professionals are supervised by our regional managers, who promote cross selling, information sharing, business referrals and high quality client service. The MMCC national network of financing professionals is supported by a dedicated, nationally focused management team coordinating access to a broad range of national and regional capital sources including bank lenders, conduit lenders, CMBS lenders, structured debt facilitators (mezzanine and preferred equity), HUD and other GSE lenders. With these resources coupled with the latest property and

13

capital markets information, we are able to access and deliver the best loan structures, financing rates and terms to meet our clients’ financial objectives.

Other Services: Research, Advisory and Consulting

Our research, advisory and consulting services are designed to assist clients in forming their investment strategy and making transaction decisions. Our advisory and consulting services are coordinated with both our investment sales and financing professionals and are designed to provide market and property focused market research, publications and customized analysis that increase customer loyalty and long-term relationships.

We also provide a wide range of advisory and consulting services to developers, lenders, owners, real estate investment trusts, high net worth individuals, pension fund advisors and other institutions. Our advisory services include opinions of value, operating and financial performance benchmarking analysis, specific asset buy-sell strategies, market and submarket analysis and ranking, portfolio strategies by property type, market strategy and development and redevelopment feasibility studies.

Seasonality

There is seasonality in our real estate brokerage commissions and financing fees, which has generally caused our revenues, operating income, net income and cash flows from operating activities to be lower in the first half of the year and higher in the second half of the year, particularly in the fourth quarter. For a more detailed description of our seasonality, refer to Item 1A – Risk Factors – External Business Risks – “Seasonal fluctuations and other market data in the investment real estate industry could adversely affect our business and make comparisons of our quarterly results difficult” and Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview – Seasonality of this Annual Report on Form 10-K.

Competition

We compete in real estate brokerage and financing within the commercial real estate industry on a national, regional and local basis. Competition is based on a number of critical factors, including the quality and expertise of our investment sales and financing professionals, our execution skills, sales support, brand recognition and our business reputation. We primarily compete with other brokerage and financing firms that seek investment brokerage and financing business from real estate owners and investors. To a lesser extent, we compete with in-house real estate departments, owners who may transact without using a brokerage firm, direct lenders, consulting firms and investment managers, some of which may have greater financial resources than we do. Our relative competitive position also varies across geographies, property types and services. In investment sales, our competitors on a national level include CBRE Group, Inc., Cushman & Wakefield, Colliers International, HFF, Inc. and Jones Lang LaSalle. Our major financing competitors include HFF, Inc., CBRE Group, Inc., Jones Lang LaSalle, Walker & Dunlop, Berkadia Commercial Mortgage LLC, Grandbridge Real Estate Capital and NorthMarq Capital, LLC. The investment sales firms mainly focus on larger sales and institutional investors and are not heavily concentrated in our largest market segment, which is the $1-$10 million private client market segment. However, there is cross over and competition between us and these firms. As a result of the fragmentation in the market, there are also numerous local and regional competitors in our markets, as well as competitors specializing in certain property types. Despite recent consolidation, the commercial real estate services industry remains highly fragmented and competitive.

Competition to attract and retain qualified professionals is also intense in each of our geographic and specialty markets. We offer what we believe to be competitive compensation and support programs to our professionals. Our ability to continue to compete effectively will depend on retaining, motivating and appropriately compensating our professionals.

14

Technology

We have a long-standing tradition of technological orientation, innovation and advancement. Our efforts include the development of proprietary applications designed to make the process of matching buyer and sellers faster and more efficient as well as state-of-the art communication technology, infrastructure, internet presence and electronic marketing.

We have a proprietary internal marketing system, MNet, which allows our salesforce to share listing information with investors across the country. MNet is an integrated tool that contains our entire national property inventory, which allows our salesforce to search for properties based on investors’ acquisition criteria. This system is an essential part of connecting buyers and sellers through our national platform. Our policies require information sharing among our salesforce, and the MNet system automates the process of matching each property we represent to the largest pool of qualified buyers tracked by our national salesforce. A part of MNet called Buyer Needs enables our salesforce to register the investment needs of various buyers which are then matched to our available inventory on a real-time basis.

We have also developed a proprietary system for automating the production of property marketing materials and launching marketing campaigns, which we call iMpact. iMpact allows our sales professionals to input data into a listing proposal or marketing package, automatically imports property information, data on comparable properties and other information, and then dynamically populates our e-marketing, print, and Internet media. This system allows our salesforce to rapidly create professionally branded and designed materials for marketing properties on behalf of our clients in an efficient and timely manner. A significant upgrade to this system is under development, which will provide updated content and expanded demographic and financial analysis to better market those properties for our clients.

We rebuilt our website in 2014 to enhance our interactions with buyers and sellers of properties. Our website is designed not only to bring in new clients for our investment sales and financing professionals, but also to make our inventory of properties available for maximum exposure for our sellers and providing buyers an opportunity to engage with our investment sales and financing professionals. We actively qualify leads generated from the contact forms, and pass those leads to our agents via our customer relationship management platform. Our website averages approximately 62,058 visitors per month (based on data from Google Analytics) and nearly 1 million page views per month (based on data from Google Analytics) and also serves as a portal for delivery of online marketing materials and for deal collaboration.

Marketing and Branding

Our 45 years of investment brokerage specialization and concentration in the $1-$10 million private client market segment have established our brand as the leading broker of investment real estate as well as a trusted source of financing solutions and market research. In recent years we have also garnered recognition among larger private investors and institutions due to our integrated platform and capability of linking private and institutional capital. We continue to strengthen and broaden the Company’s name recognition and credibility by executing a variety of marketing and branding strategies. Locally, our offices and investment sales and financing professionals engage in numerous events, direct mail campaigns, investor symposiums and participate in real estate conferences and organizations for various market segments and property types. Our regional managers and investment sales and financing professionals develop long-term client relationships and promote the Company’s brand through these activities.

Our research division produces more than 900 publications and client presentations per year and has become a leading source of information for the industry as well as the general business media. We provide research on 12 commercial property types covering: multifamily, retail, office, industrial, single-tenant net lease, seniors housing, student housing, self-storage, hospitality, medical office, manufactured housing and tax credit low income housing, as well as capital markets/financing. This research includes analysis and forecasting of the

15

economy, capital markets, real estate fundamentals, investment, pricing and yield trends, and is designed to assist investors in their strategy formation and decisions relating to specific assets and help our sales professionals develop and maintain relationships with clients.

Our transactional and market research expertise result in significant print, television and online media coverage including most major real estate publications such as GlobeStreet, Multi-Housing News, Commercial Property Executive and National Real Estate Investor as well as local market and major national news outlets such as The Wall Street Journal, The Associated Press, Reuters, Forbes, The New York Times, Los Angeles Times and the Chicago Tribune. We frequently have featured speaking roles in key regional and national industry events, and we are regularly quoted in regional and national publications and media, and deliver content directly to the real estate investment community through print, electronic publications and video. Nationally, our specialty groups and capital markets executives actively participate in various trade organizations, many of which focus on specific property types and provide an effective vehicle for client relationship development and branding.

We believe all these activities create significant exposure and name recognition for our firm which fosters and builds strong, long-term client relationships.

Intellectual Property

We hold various trademarks and trade names, which include the “Marcus & Millichap” name. Although we believe our intellectual property plays a role in maintaining our competitive position in a number of the markets that we serve, we do not believe we would be materially, adversely affected by the expiration or termination of our trademarks or trade names or the loss of any of our other intellectual property rights other than the Marcus & Millichap name. With respect to the Marcus & Millichap name, we maintain trademark registrations for these service marks.

In addition to trade names, we have developed proprietary technologies for the provision of real estate investment services, such as MNet and iMpact. We also offer proprietary research to clients through our research division. While we seek to secure our rights under applicable intellectual property protection laws in these and any other proprietary assets that we use in our business, we do not believe any of these other items of intellectual property are material to our business in the aggregate.

Government Regulation

We are subject to various real estate regulations. The Company is licensed as a mortgage broker and a real estate broker in 43 states in the United States and three provinces in Canada. We are a licensed broker in each state in which we have an office, as well as those states where we frequently do business. We are also subject to numerous other federal, state and local laws and regulations that contain general standards for, and prohibitions on, the conduct of real estate brokers and sales associates, including agency duties, collection of commissions, telemarketing, advertising and consumer disclosures.

Employees and Investment Sales and Financing Professionals

As of December 31, 2015, we had 1,607 investment sales and financing professionals of which 1,518 are exclusive independent contractors and the remainder are our employees.

We had 725 employees as of December 31, 2015, consisting of 89 financing professionals, 22 in communications and marketing, 18 in research and 596 in management and support and general and administrative functions. We believe our employee relations are good.

Most of the Company’s investment sales professionals are classified as independent contractors under state and IRS guidelines. As such, the Company generally does not pay for the professional’s expenses or benefits or

16

withhold payroll taxes; rather they are paid from the commissions earned by the Company upon the closing of a transaction, and these individuals do not earn a salary from which taxes are withheld. Almost all of the investment sales professionals hold applicable real estate broker licenses and execute a “Salespersons Agreement” setting out the relationship between the professional and the Company. Each professional is obligated to provide brokerage services exclusively to the Company, and is provided access to the Company’s information technology, research and other support and business forms. Each professional generally reports on their activities to either the local regional manager, or in some cases to product specialty managers.

Our investment sales and financing professionals are located in offices throughout the United States and Canada, each led by a regional manager with previous investment brokerage experience and an active brokerage license. We have regional managers and sales managers, who are responsible for hiring, developing and deploying sales professionals, managing regional and mid-market offices and supervising MMCC originators and support staff in their area of responsibility. We also have five group managers who oversee regional managers and multiple offices; group managers hire, develop, and support our regional managers and provide additional leadership and support for our salesforce. Finally, our management structure includes national specialty directors who lead each property type. Our national specialty directors develop our national and local brand in each property type, develop major accounts and coordinate multi-market assignments on behalf of large clients.

Traditionally, our growth has been driven by recruiting, training and developing new investment sales and financing professionals. Our new investment sales and financing professionals are trained in our technical and client service standards through a comprehensive program starting with pre-training, formal training and apprenticeship programs. While continuing to improve the recruiting, training and developing of new investment sales and financing professionals remains a major priority, we have also expanded our strategy to include more experienced investment sales and financing professionals who fit our culture and values. Over the past several years, experienced investment sales and financing professionals, including some top performers previously with national competitors, have joined the firm and have become productive members of our team. As investment sales and financing professionals mature, we continue with specialized training and best practices sessions by tenure, which are conducted by senior management, regional managers, leading sales professionals and our national specialty directors. The goal of this rigorous approach to training is to continually improve our team’s skill set and client services. Our salesforce conducts business the same way across the country to deliver a high level of consistency, professionalism and reliability to our clients who often buy and sell investments in variety of property types and locations.

Our investment sales and financing professionals receive a percentage of the commission received by the Company. As investment sales and financing professionals become more senior, they receive a larger percentage of the commission based on tenure and production. Depending on the aggregate gross commissions, a portion of the investment sales and financing professional’s commission may be deferred for three years.

Emerging Growth Company Status

We currently are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes Oxley Act of 2002, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

We have irrevocably elected to opt out of the extended transition period for complying with new or revised accounting standards pursuant to Section 107(b) of the JOBS Act, and therefore, we are subject to the same new or revised accounting standards as other public companies that are not “emerging growth companies.”

17

We could remain an “emerging growth company” for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period.

Available Information

Our website address is www.marcusmillichap.com. Information on our website does not constitute part of this report and inclusions of our internet address in this Annual Report on Form 10-K are inactive textual references only. We are required to file current, annual and quarterly reports, proxy statements and other information required by the Exchange Act, with the SEC. We make available free of charge through a link provided on our website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, Forms 3, 4 and 5 filed by or on behalf of directors, executive officers and certain large stockholders, and any amendments to those documents filed or furnished pursuant to the Exchange Act. Such reports are available as soon as reasonably practicable after they are filed with the SEC.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website that contains reports, proxy and information statements and other information regarding the Company that we file electronically with the SEC at www.sec.gov.

We also make available on our website and will provide print copies to stockholders upon request, (i) our corporate governance guidelines, (ii) our code of ethics, and (iii) charters of the audit, compensation, corporate governance and nominating committees of our board of directors.

From time to time, we may announce key information in compliance with Regulation FD by disclosing that information on our website.

18

Investing in our securities involves a high degree of risk. You should consider carefully the following risk factors and the other information in this Annual Report on Form 10-K, including our consolidated financial statements and related notes, before making any investment decisions regarding our securities. If any of the following risks actually occur, our business, financial condition and operating results could be adversely affected. As a result, the trading price of our securities could decline and you may lose part or all of your investment.

Overview

We are impacted by and manage many risk factors detailed below affecting our business including External Business Risks, Human Resource and Personnel Risks, Internal Business Risks, and Risks related to the Ownership of Our Common Stock. Many of these factors described below in External Business Risk, are outside of our control. In addition, we are a personnel and relationship intensive business rather than a capital intensive business. While all the risk factors discussed below have the potential to negatively impact our business, the most significant risks facing the Company are the general economic conditions and commercial real estate market conditions risk and our ability to attract and retain qualified and experienced managers and investment sales and financing professionals.

External Business Risks

General economic conditions and commercial real estate market conditions have had and may in the future have a negative impact on our business.

We may be negatively impacted by periods of economic slowdowns, recessions and disruptions in the capital markets; credit and liquidity issues in the capital markets, including international, national, regional and local markets; and corresponding declines in the demand for commercial real estate investment and related services. Historically, commercial real estate markets, and in particular the U.S. commercial real estate market, have tended to be cyclical and related to the flow of capital to the sector, the condition of the economy as a whole and to the perceptions and confidence of the market participants as to the relevant economic outlook. Cyclicality in the real estate markets may lead to cyclicality in our earnings and significant volatility in our stock price. Real estate markets may “lag” the broader economy. This means that even when underlying economic fundamentals improve in a given market, it may take additional time for these improvements to translate into strength in the real estate markets. The “lag” may be exacerbated when banks delay their resolution of commercial real estate assets whose values are less than their associated loans.

Negative economic conditions, changes in interest rates, credit and liquidity issues in the capital markets, disruptions in capital markets and/or declines in the demand for commercial real estate investment and related services in international and domestic markets or in significant markets in which we do business, have had and could have in the future a material adverse effect on our business, results of operations and/or financial condition. In particular, the commercial real estate market is directly impacted by the lack of debt and/or equity for commercial real estate transactions, increased interest rates and changes in monetary policies by the Federal Reserve, changes in the perception that commercial real estate is an accepted asset class for portfolio diversification, and slowdowns in economic activity that could cause residential and commercial tenant demand to decline, which would adversely affect the operation and income of commercial real estate properties.

These and other types of events could lead to a decline in transaction activity as well as a decrease in values, which would likely in turn lead to a reduction in brokerage commissions and financing fees relating to such transactions. These effects would likely cause us to realize lower revenues from our transaction service fees, including investment sales commissions, which fees usually are tied to the transaction value and are payable upon the successful completion of a particular transaction. Such declines in transaction activity and value would likely also significantly reduce our financing activities and revenues. For example, the disruptions and

19

dislocations in the global credit markets during 2008 and 2009 created significant restrictions in the availability of credit, especially on transitional assets and in the secondary and tertiary markets. In turn, the volume and pace of commercial real estate transactions were significantly reduced, as were property values, which generally peaked in 2007 and fell through 2010.

Fiscal uncertainty as well as significant changes and volatility in the financial markets and business environment, and in the global political, security and competitive landscape, make it increasingly difficult for us to predict our revenue and earnings into the future. As a result, any revenue or earnings guidance or outlook which we might give may be overtaken by events or may otherwise turn out to be inaccurate.

We have numerous significant competitors and potential future competitors, some of which may have greater resources than we do, and we may not be able to continue to compete effectively.

We compete in investment sales and financing within the commercial real estate industry. Our investment sales focus is on the private client market segment, which is highly fragmented. The fragmentation of our market makes it challenging to effectively gain market share. While we have a competitive advantage over other national firms in the private investor segment, we also face competition from local and regional service providers who have existing relationships with potential clients. Furthermore, transactions in the private investor segment are smaller than many other commercial real estate transactions. Although the brokerage commissions in this segment are generally a higher percentage of the sales price, the smaller size of the transactions requires us to close many more transactions to sustain revenues. If the commission structure or the velocity of transactions were to change, we could be disproportionately affected by changes compared to other companies that focus on larger transactions, institutional clients and other segments of the commercial real estate market.

There is no assurance that we will be able to continue to compete effectively or maintain our current fee arrangements with our private clients or margin levels or we will not encounter increased competition. The services we provide to our clients are highly competitive on a national, regional and local level. Depending on the geography, property type or service, we face competition from, including, but not limited to, commercial real estate service providers, in-house real estate departments, private owners and developers, commercial mortgage servicers, institutional lenders, research and consulting firms, and investment managers, some of whom are clients and many of whom may have greater financial resources than we do. In addition, future changes in laws and regulations could lead to the entry of other competitors. Many of our competitors are local, regional or national firms. Although most are substantially smaller than we are, some of these competitors are larger on a local, regional or national basis, and we believe more national firms are exploring entry into or expansion in the $1-$10 million private client market segment. We may face increased competition from even stronger competitors in the future due to a trend toward acquisitions and consolidation. We are also subject to competition from other large national and multi-national firms as well as regional and local firms that have similar service competencies to ours. Our existing and future competitors may choose to undercut our fees, increase the levels of compensation they are willing to pay to their employees and investment sales and financing professionals, and either recruit our employees and investment sales and financing professionals or cause us to increase our level of compensation necessary to retain employees or investment sales and financing professionals, or recruit new employees or investment sales and financing professionals. These occurrences could cause our revenue to decrease, which could have an adverse effect on our business, financial condition and results of operations.

Our brokerage operations are subject to geographic and commercial real estate market risks, which could adversely affect our revenues and profitability.

Our real estate brokerage offices are located in and around large metropolitan areas as well as mid-market regions throughout the United States and Canada. Local and regional economic conditions in these locations could differ materially from prevailing conditions in other parts of the country. We have more offices and realize more of our revenues in California, the Midwest, the Northeast and the Southeast. In 2015, we earned approximately 31%, 17%, 14% and 13% in California, the Midwest, the Southeast and the Northeast,

20

respectively. In particular, we are subject to risks related to the California economy and real estate markets. In addition to economic conditions, this geographic concentration means that California-specific legislation, taxes and regional disasters such as earthquakes could disproportionately affect us. A downturn in investment real estate demand or economic conditions in these regions could result in a further decline in our total gross commission income and profitability and have a material adverse effect on us.

Seasonal fluctuations and other market data in the investment real estate industry could adversely affect our business and make comparisons of our quarterly results difficult.

Our revenue and profits have historically tended to be significantly higher in the fourth quarter of each year than in the first quarter. This is a result of a general focus in the real estate industry on completing or documenting transactions by calendar year end and because certain expenses are constant throughout the year. Historically, we have reported relatively lower earnings in the first quarter and then increasingly larger earnings during each of the following three quarters. This historical trend can be disrupted both positively and negatively by major economic or political events impacting investor sentiment for a particular property type or location, volatility in the stock market, current and future projections of interest rates, attractiveness of other asset classes, market liquidity and the extent of limitations or availability of capital allocations for larger institutional buyers, to name a few. As a result, our historical pattern of seasonality may or may not continue to the same degree experienced in the prior years and may make it difficult to determine during the course of the year whether planned results will be achieved, and thus to adjust to changes in expectations.

A change in the tax laws relating to like-kind exchanges could adversely affect our business and the value of our stock.

Section 1031 of the Internal Revenue Code of 1986, as amended (the “Code”), provides for tax-free exchanges of real property for other real property. Legislation has been proposed on several occasions that would repeal or restrict the application of Section 1031. If tax-free exchanges under Section 1031 were to be limited or unavailable, our clients or prospective clients may decide not to purchase or sell property that they would have otherwise purchased or sold due to the tax consequences of the transaction, thus reducing the commissions we would have otherwise received. Any repeal or significant change in the tax rules pertaining to like-kind exchanges could have a substantial adverse impact on our business and the value of our stock.

The Internet could devalue our information services and lead to reduced client relationships, which could reduce the demand for our services.